ACOs at a Crossroads: Costs, Risk and MACRA

A NAACOS Policy White Paper

Authors: Allison Brennan, Vice-President of Policy and Clif Gaus, President and CEO, National Association of ACOs

Executive Summary

Introduction

ACO Risk Models

ACO Costs and Investments

ACOs and MACRA

Overlap of ACOs and Bundled Payments

Summary of Policy Recommendations and Conclusion

Appendix A: ACO Risk Structures

Executive Summary

This white paper is designed to call attention to the significant challenges facing accountable care organizations (ACOs) as they prepare for a new reality in Medicare and the rapidly evolving health care industry. ACOs represent a refined approach to the delivery of health care and were created to facilitate coordination and cooperation among providers to improve the quality of care and to reduce unnecessary costs. Although the ACO model holds great promise, Medicare ACOs are at a crossroads. After initial rapid growth in the Medicare Shared Savings Program (MSSP) and strong commitments from ACOs to a model that can transform care delivery, recent policy decisions by the Centers for Medicare & Medicaid Services (CMS) and the Administration could significantly undercut the ability of ACOs to flourish individually and collectively. Should the Administration remain on its current policy trajectory, Medicare ACOs may be destined to decline over time, precipitating the end of today’s ACOs.

The National Association of ACOs (NAACOS) is the largest association of Medicare ACOs, representing over 3 million beneficiary lives through 180 MSSP ACOs, Next Generation, Pioneer and commercial ACOs. NAACOS is an ACO member-led and member-owned non-profit organization that works on behalf of ACOs across the nation to improve the quality of Medicare delivery, population health and outcomes, and health care cost efficiency. This white paper details key challenges for ACOs and suggests solutions to address them in a way that would strengthen ACOs and ensure their long-term viability. NAACOS recently conducted a survey of MSSP ACOs on their costs, ability to take on risk, and feedback on implementation of the Medicare Access and CHIP Reauthorization Act (MACRA) and, as seen later in this document, the findings are compelling. This white paper incorporates the survey findings along with NAACOS’s policy recommendations, including requests that CMS and the Administration take immediate action to:

- Account for the significant investments ACOs make by including them in calculations of ACO risk,

- Address shortcomings of existing ACO two-sided risk models which require levels of financial risk that are untenable for many ACOs,

- Include all ACOs in CMS’s list of Advanced Alternative Payment Models (APMs) under MACRA, and

- Remedy issues related to the overlap of competing CMS programs in a way that prioritizes population-based payment models such as ACOs.

As we have seen, it is a long, heavy lift for many ACOs to achieve early success, which is necessary to enable their continued participation and prepare them to migrate to risk-based models. ACOs are on the cusp of so much potential, and we hope this white paper starts a dialogue about these issues so we can work together to support ACOs today and moving into the future.

Introduction

As Medicare evolves from paying health care providers based on volume to value, the MSSP and other Medicare ACO models, such as Next Generation ACOs, will play a critical role in improving care for individuals, enhancing the health of populations, and slowing the growth rate in Medicare expenditures. Established by the Patient Protection and Affordable Care Act (ACA), MSSP ACOs are a key component of the Medicare delivery system reform initiatives included in the ACA and further emphasized in the MACRA. The ACO model has broad bipartisan support and has evolved in the past decade since the Physician Group Practice Demonstration, which began during the Bush Administration and was the first pay-for-performance program upon which current models are based.

To better understand and quantify ACO investments, costs and their perspectives on MACRA implementation, NAACOS recently conducted a survey of 2015 and 2016 MSSP ACOs, which includes ACOs that began the program as early as 2012. Out of 433 ACOs in the MSSP, 144 unique ACOs responded to the 13-question survey and provided their perspectives and cost data. Some of the feedback and results are included in this white paper and a comprehensive survey report is available here. The survey respondents included a variety of ACOs, based on size, MSSP start year, ACO structure, and geographic representation across 40 states, reflecting the broad range of MSSP ACOs.

ACOs face serious challenges, including difficulties taking on downside risk as still young and developing organizations, CMS’s unwillingness to recognize and reward the significant investments ACOs make, and new CMS programs that compete with and hinder ACO growth and ability to succeed. Additionally, recent CMS proposals to exclude MSSP Track 1 ACOs as Advanced APMs under MACRA further shakes the confidence that ACOs, medical groups, and hospitals have in Medicare’s dedication to this care delivery model.

The white paper will discuss the background and issues for each of the following concerns and conclude with recommendations:

- ACO risk models

- ACO cost and investment

- ACOs and MACRA

- Overlap of ACOs and bundled payments

- NAACOS recommendations

ACO Risk Models

ACO Risk Models: Background and Issues

Early in the process, ACOs apply to CMS for a specific model, which originally included the Pioneer ACO model or MSSP, and within the MSSP they apply for a particular track. The MSSP originally included two tracks, and CMS introduced MSSP Track 3 and the Next Generation ACO model in 2016. Track 1 of the MSSP is the only one that has no downside risk for the ACO except for the startup and operational expenses. This track is known as a one-sided model. Under current policy, ACOs may remain in Track 1 for up to six years (for two three-year agreement periods). Since inception of the MSSP, CMS has emphasized the need for ACOs to assume downside financial risk for their patient population. Policymakers encourage this “skin in the game,” which they argue is the best way to incentivize ACOs to reduce unnecessary utilization and lower the growth rate of Medicare expenditures. The current ACO models vary based on their risk structures, which are outlined in Appendix A, and the main components of two-sided risk include:

- Minimum loss rate (MLR): apercentage by which actual expenditures may exceed expected expenditures without triggering financial risk. If an ACO is at or above their MLR, it is required to repay Medicare for a portion of the losses.

- Shared loss rate: the percentage of the amount by which actual expenditures exceed expected expenditures for which an ACO would be held liable. This rate determines what portion of the losses the ACO would have to pay back, should its losses meet or exceed the MLR.

- Loss sharing limit: a cap on losses, which is the maximum potential payment for which an ACO can be held liable. This cap is a percent of the ACO’s benchmark.

ACOs in two-sided models that have losses exceeding their MLR are required to repay a portion of the losses to Medicare, based on their shared loss rate. That sharing rate ranges from as low as 40 percent for some ACOs in Tracks 2 or 3 up to 100 percent for some ACOs in the Next Generation model. The total amount of losses is capped based on the ACO’s loss sharing limit, which ranges from as low as five percent in Year 1 for Track 2 ACOs to 15 percent for Tracks 3, Next Generation and Pioneer ACOs. The loss sharing limit is based on total cost of care, which is also used to determine ACO financial benchmarks and whether the ACO will share in any savings or losses.

To entice ACOs to participate in two-sided risk models, CMS provides them with higher shared savings rates, meaning successful ACOs get to keep more of the money they help save. MSSP Tracks 2 and 3 have shared savings rates of up to 60 and 75 percent, respectively, and the Next Generation model offers shared savings rates between 80 and 100 percent. Higher shared savings rates are favorable for ACOs but mean the government and the Medicare Trust Finds receive a lower portion of savings. CMS also allows MSSP Track 3, Next Generation and Pioneer ACOs to have prospective beneficiary assignment, meaning they know up front who their ACO beneficiaries are, which helps them understand more about their beneficiary population and results in more stable financial benchmarks. Further, in some instances CMS provides two-sided ACOs with waivers related to certain Medicare rules, which allows them greater flexibility to provide services such as telehealth or home health or to reward beneficiaries for staying in the ACO’s network.

ACO Risk Models: Participation in Two-Sided Risk

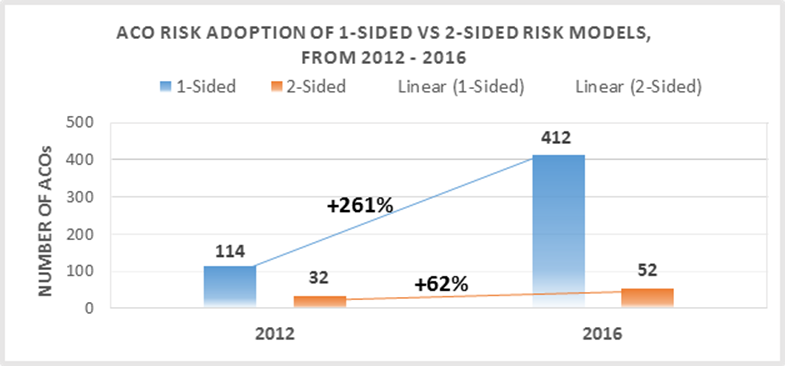

To date, the growth rate in two-sided risk models (MSSP Tracks 2 and 3, the Pioneer ACO model, and Next Generation ACO model) has been unimpressive, as shown in Figure 1 below. Further, as a portion of total 2016 Medicare ACOs, those in two-sided risk models only represent slightly more than 10 percent of total ACOs. On the other hand, from 2012 to 2016 the growth rate for Track 1 is four times the growth rate of two-sided models and remains by far the most popular option.

ACO Risk Models: Early Results of Two-Sided Models

To date, results of two-sided ACO models have been mixed while participation in these models continues to wane. For participation from 2012 through 2014, the relatively small cohort of two-sided ACOs had to repay CMS a total of $30,219,738. This includes both MSSP Track 2 ACOs and Pioneer ACO participants during this time frame. Losses for these organizations ranged from $1,037,260 to $4,767,562 (repaid losses paid on an annual basis). In 2014 alone, three Pioneer ACOs had to repay CMS close to $9 million. As a result of losses and other program challenges, two-sided ACO programs have seen high dropout rates. The Pioneer program is the best example of this, beginning in 2012 with 32 participants and only 9 remaining participants in 2016. MSSP Track 2 ACOs also saw a 50 percent dropout rate between 2011 and 2015. This highlights the hazardous nature of physician involvement in downside risk arrangements.

ACO Risk Models: Challenges Taking on Two-Sided Risk

The limited uptake and early performance results of two-sided ACOs demonstrate that the economics of the current two-sided models are impractical. For many ACOs, a key determination is whether the ACO can commit to repaying CMS for losses incurred treating Medicare beneficiaries if the ACO’s actual costs exceed projections by more than a certain percent. The decision to take on risk is often at the heart of an ACO’s choice about which model to select. Despite policymakers’ earnest desire to attract ACOs to these models, that optimism cannot outweigh the realities ACOs face as they carefully consider the requirements for taking on two-sided risk. Having to potentially pay millions of dollars to Medicare is simply not practical nor feasible for these organizations. This type of risk often necessitates that ACOs have considerable financial backing, which is why, for the most part, these models have attracted ACOs with hospitals, health systems or outside investors.

While larger hospitals are likely to have greater assets and access to substantial lines of credit compared to smaller independent medical groups, they must be careful to properly evaluate the risks to the downside on both their bond ratings and their long-term financial viability. According to research conducted by the American Hospital Association, the average hospital operating margin has been trending between five and seven percent in recent years. This contributes to a general reluctance to take on significant exposure to downside risk. Further, smaller or more rural hospitals and most independent medical groups are unable to access investor capital and face many barriers to obtaining sizeable credit. Without assets large enough to secure loans, many physician owners are left having to personally guarantee debts and obligations. Smaller, physician-led ACOs have been even more reluctant to add this level of risk to their balance sheet as they could not sustain the potential losses CMS requires them to protect against.

To understand the current risk models, we’ll use an example of a hypothetical ACO with 300 primary care physicians caring for 10,000 Medicare beneficiaries and a total benchmark of $100,000,000. On a national basis, all physician professional services comprise 19 percent of total Medicare Parts A and B spending. However, that includes all specialty and hospital-based physicians, which are paid more than primary care physicians who typically comprise the majority of an ACO’s physicians. Further, most ACOs are organized and governed by a majority of primary care physicians so the physician spending is a far less percentage of total patient costs. It is common for an ACO’s physicians, those assuming financial responsibility for the total cost of the ACO’s attributed beneficiaries, to have Medicare gross billings comprising about 10 percent of total costs. Therefore, in our example below, we assume gross Medicare income would be $10,000,000.

However, that gross income goes toward more than just physician salaries. In fact, according to the final 2015 Medicare Physician Fee Schedule, only about 50 percent of Medicare payment relates to physician work while 45 percent helps cover practice expenses such as building costs, equipment and staff salaries, and approximately five percent goes towards covering malpractice insurance. Therefore, that leaves the physicians an actual net income closer to $5,000,000, as seen in Table 1 below.

Table 1: Example of a hypothetical MSSP ACO.

| Physicians | Beneficiaries | Cost per Beneficiary | Total Benchmark | Medical Group Gross Income | Physician Income |

| 300 | 10,000 | $10,000 | $100,000,000 | $10,000,000 | $5,000,000 |

Under the first performance year of MSSP Track 2 (the lowest risk of any model for any year), an ACO is responsible for losses of up to five percent of its total benchmark, which increases to 10 percent by performance year three. Table 2 below illustrates how that translates into risk for the ACO owners. Therefore, under the smallest amount of risk in a Medicare two-sided risk model, CMS requires ACO physicians to be liable for an amount equivalent to their entire Medicare net income.

Table 2: ACO Owner Risk

| Benchmark | Year 1 Loss Sharing Limit | Year 3 Loss Sharing Limit |

| $100,000,000 | $5,000,000 | $10,000,000 |

Basing risk on total cost of care creates situations where physicians could be responsible for repaying a substantial amount, if not all, of their Medicare income, and such high risk in not feasible for the vast majority of ACO physician owners. The challenges of taking on risk are often exacerbated in rural areas where ACOs tend to have even fewer resources and may struggle to come up with start-up and investment costs, let alone be in a position to assume down-side risk. Even the promise of higher sharing rates or the ability to utilize waivers afforded to two-sided ACOs is not enough to overcome the barriers to assuming financial risk. Further, ACOs are in the business of delivering care and are not necessarily well equipped to take on what is essentially actuarial risk more typical of a health insurance company than a physician practice. Finally, while a slight majority of ACOs are physician owned, many others share ownership and financial responsibility with hospitals. The hospitals often have the same concerns about sharing in this level of risk as well.

ACO Risk Models: Survey Results on Two-Sided Risk

For ACOs to move successfully through the risk continuum, most begin with Track 1, in which about 90 percent of ACOs currently operate. It is a long, heavy lift for many ACOs to achieve success in Track 1 before they are ready to migrate into higher risk tracks. One of the goals of our recent NAACOS ACO Cost and MACRA Implementation Survey was to better understand ACOs’ willingness and ability to assume financial risk under a two-sided model. (Please refer to our comprehensive survey report for a full description of the survey methodology and findings.) All ACOs participating in the MSSP in 2015 and 2016 received an email with information about the survey, which includes ACOs that began the program as early as 2012.

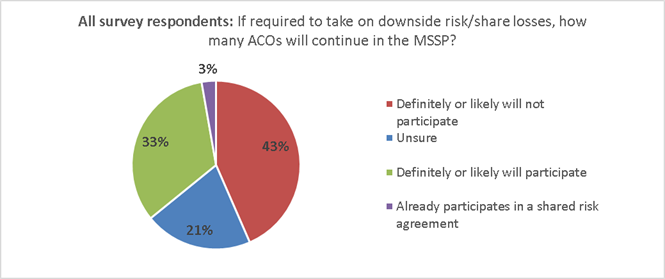

One of the key takeaways from the survey is that ACOs are not currently prepared to take on the significant financial risk required in the current two-sided risk models. As seen in Figure 2 on the following page, when asked how likely the ACO is to continue participating in the MSSP if CMS requires downside risk, less than half (43 percent) said they definitely or likely will not continue in the MSSP. Twenty-one percent were unsure, and a third will definitely or likely continue to participate.

Figure 2: Survey response to “How likely is your ACO to participate in the MSSP if CMS requires ACOs to share losses?”

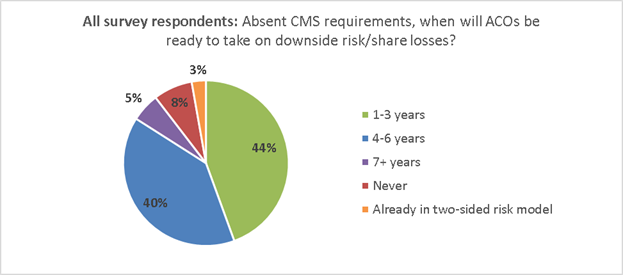

While many ACOs do not feel ready to take on risk now, most may be prepared to do so in the future. When asked how many years until an ACO is willing to take on downside risk, 84 percent said within the next six years (44 percent within 1-3 years and 40 percent within 4-6 years), as seen in Figure 3 below.

Figure 3: Survey repsonse to “Absent any CMS requirements to do so, indicate your best estimate for how many years it would be before your ACO would be willing to share losses.

While the data shows that a small portion of ACOs feel they will never be able to take on risk, it is promising that within six years, a large majority of ACOs believe they will be ready to move to two-sided models. However, this question did not ask about the specific level of risk in two-sided ACO risk models, and many survey respondents also commented that they are very concerned about the amount of risk required in the current Medicare two-sided models. As one survey respondent commented, “We would like to see a pathway to risk sharing that allows us to build the necessary reserves.”

ACO Costs and Investments

ACO Costs and Investments: Background and Issues

The majority of ACOs are reluctant to participate in two-sided risk models largely due to the financial risk required and the considerable investments in their ACO. Because these investments do not guarantee shared savings, ACOs view them as risk inherent in MSSP participation. These investments include start-up and operating costs. Our survey included questions about these costs, breaking them down into four categories detailed in Table 3 below.

Table 3: Survey responses to “Provide estimated marginal operating costs attributable to your participation in the MSSP.”

| Estimated ACO Operating Costs: | Total Averages: |

| Clinical and care management | $642,044 |

| Health care information technology, population analytics, and reporting | $501,300 |

| ACO management, administration, financial, legal, and compliance | $402,272 |

| Other (sum or all other operating costs) | $121,115 |

| Total operational costs: | $1,622,032 |

The survey respondents were broken into ACOs who are either independent entities or are part of a group with centralized operations and other shared services among many ACOs. These two groups were categorized as single ACOs or multi-ACOs respectively. Out of the survey respondents, 70 percent represent single ACOs and 30 percent represent multi-ACOs. Interestingly, the difference in operating costs between the single and multi-ACOs is almost half. The average cost of single ACOs is almost $2 million ($1,943,276), whereas the average cost of multi-ACOs is almost $1 million ($974,289) and the mean average for all survey respondents is between both of those amounts at $1,622,032. The range across all of the survey respondents is significant, ranging from as low as $185,000 to as much as $9,500,000.

In addition to the quantitative data survey respondents provided on costs, they also shared their feedback on these costs:

“We believe that there is considerable risk for ACOs that are participating in the one-sided model. The risk is inherent in the investments the ACOs are making in people to deliver the care/services to patients along with the technological and support costs that they may never see a return. If there never was participation in such an agreement these costs would not be incurred.”

“Our ACO is physician-owned and funded. Raising capital to develop our infrastructure has not been easy and comes at a substantial cost. Despite no downside risk from CMS, the risk of loss from personal investment is substantial.”

Despite repeated calls to do so, CMS unfortunately refuses to give ACOs credit for these investments or count them as financial risk. For example, in the May 9 MACRA Notice of Proposed Rule-Making (NPRM), the agency states:

“Many stakeholders commented that business risk should be sufficient to meet this financial risk criterion to be an Advanced APM. We also considered whether the substantial time and money commitments required by participation in certain APMs would be sufficient to meet this financial risk criterion. However, we believe that financial risk for monetary losses under an APM must be tied to performance under the model as opposed to indirect losses related to financial investments APM Entities may make. The amount of financial investment made by APM Entities may vary widely and may also be difficult to quantify, resulting in uncertainty regarding whether an APM Entity had exceeded the nominal amount required by statute.” (MACRA NPRM, 81 Fed. Reg. 89, May 9, 2016).

We understand the variability of these investments, which can be influenced by characteristics such as ACO size, structure, experience with population health payment models, or funding available to the ACO. However, based on our survey response rate of 33 percent of participating 2015 and 2016 ACOs, we feel confident in the average estimate of $1.6 million in annual operating costs. This figure also aligns with CMS’s own previous estimates. In the November 2011 Final ACO Rule, CMS stated:

“In order to participate in the program, we realize that there will be costs borne in building the organizational, financial and legal infrastructure that is required of an ACO as well as performing the tasks required (as discussed throughout the Preamble) of an eligible ACO, such as: Quality reporting, conducting patient surveys, and investment in infrastructure for effective care coordination.” (Final ACO Rule, 76 Fed. Reg. 212, November 2, 2011).

“Our cost estimates for purposes of this final rule reflect an average estimate of $0.58 million for the start-up investment costs and $1.27 million in ongoing annual operating costs for an ACO participant in the Shared Savings Program” (Final ACO Rule, 76 Fed. Reg. 212, November 2, 2011).

CMS based these estimates in part on those related to the Physician Group Practice (PGP) Demonstration, a precursor to the MSSP that ran from 2005 to 2010. In the November 2011 Final ACO Rule, CMS explained:

“An analysis produced by the Government Accountability Office (GAO) of first year total operating expenditures for participants of the Medicare PGP Demonstration varied greatly from $436,386 to $2,922,820 with the average for a physician group at $1,265,897 (Medicare Physician Payment: Care Coordination Programs Used in Demonstration Show Promise, but Wider Use of Payment Approach May Be Limited. GAO, February 2008)”. (Final ACO Rule, 76 Fed. Reg. 212, November 2, 2011) “We continue to believe that the structure, maturity, and thus associated costs represented by those participants in the Medicare PGP Demonstration are most likely to represent the majority of anticipated ACOs participating in the Shared Savings Program.” (Final ACO Rule, 76 Fed. Reg. 212, November 2, 2011)

When adjusting for inflation using the Department of Labor Consumer Price Index inflation calculator, the average estimate in the November 2011 Final ACO Rule for ACOs in the MSSP would be $1,350,867, and adjusting the GAO average estimate for PGP participants in the first year of that program, 2005, would result in $1,550,844. These estimates closely align with the results from our survey. With repeated estimates that provide similar results, it is difficult to see how CMS can continue to ignore these costs and not consider them as risk for the ACO.

ACOs and MACRA

CMS’s MACRA Proposal to Exclude Track 1 ACOs from Advanced APMs: Background and Issues

Passed in 2015, MACRA sets Medicare physician payment on a new course with two paths: one for providers in eligible APMs, and the other for those who do not meet the eligible APM criteria requires participation in the Merit-Based Incentive Payment System (MIPS). From 2019 through 2024, qualifying participants (QPs) in eligible APMs will earn annual lump sum bonuses of 5 percent (based on estimated aggregate payment amounts for covered professional services under the Medicare Physician Fee Schedule from the previous year). Beginning in 2026, the Medicare update factor for those in eligible APMs will be 0.75 percent annually, compared to a 0.25 percent for those in MIPS. The five percent APM bonus and 0.75 percent update amount are separate from any bonuses or penalties resulting from participation and performance in the specific eligible APM. MIPS has separate payment adjustments which begin in 2019 with maximum bonuses/penalties of four percent, which increase over time to nine percent beginning in 2022 and beyond.

MACRA defines an APM as any of the following:

- A model under the Center for Medicaid and Medicare Innovation (other than a health care innovation award)

- An MSSP ACO

- A demonstration under Section 1866C of the Social Security Act

- A demonstration required by federal law

As a subset of APMs, MACRA eligible APMs must meet the following criteria:

- Provide for payment for covered professional services based on quality measures comparable to those under MIPS

- Require use of certified electronic health records (EHRs)

- Bear more than nominal financial risk or be a medical home model

Those in eligible APMs must also meet thresholds based on a portion of Medicare payments or patients to qualify for the APM bonus. For example, in 2019 and 2020 at least 25 percent of Medicare payments must be attributable to services furnished to Medicare beneficiaries through an eligible APM or at least 20 percent of the APM’s patients must be attributed to the APM. These thresholds increase over time.

In the MACRA NPRM released in the Federal Register May 9, 2016, CMS proposes key details to implement APMs and MIPS. In the MACRA NPRM, CMS introduces the term “Advanced APM,” which the agency uses in place of “eligible APM,” as referred to in the MACRA statute. The departure from “eligible APM” to “Advanced APM” is notable because CMS raises the bar considerably with its definition of an Advanced APM, going much further than required by statute. In fact, CMS’s proposed criteria for what qualifies as an Advanced APM is so stringent that, if finalized, only six APMs would be considered Advanced APMs and earn the five percent eligible APM bonus. MSSP Tracks 2 and 3 and Next Generation ACOs are included on CMS’s proposed list of Advanced APMs, but Track 1 of the MSSP is excluded. The APM model (e.g., MSSP Track 3) is the Advanced APM and within the model, an individual participant (e.g., America ACO) is considered an Advanced APM Entity.

CMS’s proposal for what it means to “bear more than nominal financial risk” is at the heart of what determines whether an APM qualifies as an Advanced APM. CMS’s definition would require that if an Advanced APM Entity’s actual expenditures for which it is responsible exceed expected expenditures during a specified performance period, CMS can:

- Withhold payment for services to the APM Entity and/or the APM Entity’s eligible clinicians

- Reduce payment rates to the APM Entity and/or the APM Entity’s eligible clinicians or

- Require the APM Entity to owe payment(s) to CMS.

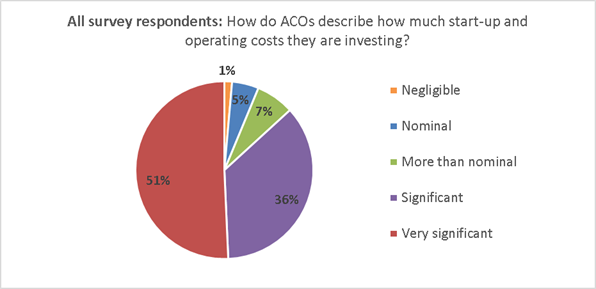

With this definition that excludes 90 percent of ACOs as Advanced APMs., CMS once again ignores the significant investments ACOs make to participate. While CMS continues to disregard these investments, ACOs argue their importance. In fact, when asked to describe their investments, over half (51 percent) of the respondents said that their ACO’s investment is “very significant,” as seen in Figure 4 on the following page.

Figure 4: Survey response to “Which word or phrase best describes your perspective regarding the investments your ACO has made (including both start-up and ongoing operating costs) to participate in the MSSP?”

Many survey respondents further elaborated on this, including this particular comment:

“We think the ACO is a good opportunity for us to transform how care is provided in our community to meet the health care needs of the future. We are all making significant sacrifices to put this organization together, both in personal finances and time. CMS needs to take into consideration the personal risks we are taking in addition to the definable financial risks.”

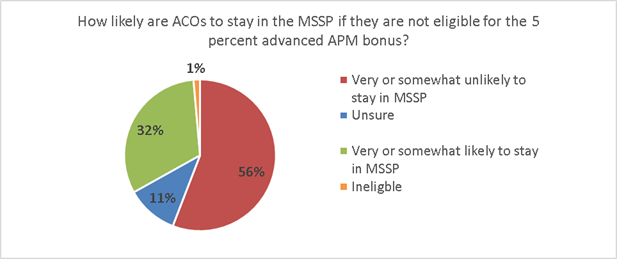

To better understand how ACOs may respond to MACRA and CMS’s approach to defining eligible or Advanced APMs, our survey asked how likely ACOs would be to stay in the MSSP if they are not eligible for the five percent Advanced APM bonus. As illustrated in Figure 5 below, 56 percent of the ACOs responded that they would leave the MSSP.

Figure 5: Survey repsonse to “How likely is it that your ACO would stay in the Medicare Shared Savings Program (MSSP) if Track 1 ACOs were not eligible for the APM 5 percent bonus?”

Overlap of ACOs and Bundled Payments

Bundled Payment Programs: Background and Issues

The prevalence of Medicare bundled payment programs has grown considerably in the last few years. In these models, hospitals, physician groups, or post-acute care providers bear financial risk for spending during an episode of care relative to a “target price,” often based on their historical spending for an episode minus a small discount, such as 2 or 3 percent. In an ideal world, there would be opportunities for both population-based payment models such as ACOs and bundled payment models to co-exist and even support one another. Unfortunately, in reality these models often compete with one another, and depending on how CMS chooses to address their overlap, that competition could harm ACOs and significantly weaken their ability to succeed as a payment model. Conflicts arise when patients attributed to an ACO are also evaluated under a bundled payment program. Under CMS policy, the bundled payment participant maintains financial responsibility for the bundled payment episode of care and any gains or losses during that episode are linked to the bundled payment participant and are removed from ACO results during year-end financial reconciliation.

The Medicare Bundled Payments for Care Improvement (BPCI) and the Comprehensive Care for Joint Replacement (CJR) Model are two premier CMS bundled payment programs. The BPCI initiative began in 2013 and, according to the CMS BPCI webpage, as of April 1 includes 1,522 participants. Under BPCI, participants elect to be paid a bundled price for up to 48 defined clinical episodes. There are four models within BPCI. The most popular are: (1) Model 2 with bundles that begin with a hospitalization and include all related services for up to 90 days after discharge and (2) Model 3 with bundles that begin with admission to a post-acute care facility or home health care. Total BPCI spending most likely exceeds $10 billion annually.

The CJR Model focuses on bundled payments to acute care hospitals for hip and knee replacement surgery, with an episode of care beginning when a Medicare fee-for-service beneficiary is admitted to a participant hospital and lasting through 90 days post-discharge. Notably, this bundled payment program is mandatory for hospitals in select geographic areas and is the first required program of this type and scale. CJR includes participant hospitals located in 67 Metropolitan Statistical Areas throughout the country. CMS indicates that approximately 800 hospitals will be required to participate in the model, which began April 1, 2016 and will run through 2020. CJR is expected to account for $2.5 billion to $3 billion in annual payments.

When CMS calculates an ACO’s shared savings, the spending for ACO patients with an episode of care provided by a bundled payment participant is set to that bundler’s target price, regardless of actual spending. Target prices based on higher cost baselines arbitrarily raise an ACO’s performance cost and removes their saving opportunity. However, certain ACOs can benefit from bundled payment program overlap if a bundle target price is lower than the ACO’s actual spending. While this impact may be favorable or unfavorable for a particular ACO depending on their costs relative to those of the bundler(s) in their market, the net effect skews accountability for population-based models and in general undermines ACOs’ opportunity for savings through care redesign since any savings would automatically go to the bundler. The problem is further exacerbated by the fact that the 60 to 90-day patient episode of care is carved out of the ACO’s provider network and there are no requirements for the bundler to transition the patient or their medical records back to the ACO to which they are assigned.CMS argues that prioritizing bundled payment programs helps assure adequate sample size for bundlers. However, much of the variation in per-episode spending is a result of utilization of post-acute care or readmissions, both of which ACOs are often instrumental in managing or preventing. ACOs focus on, and make considerable investments in, care coordination and improving care transitions to manage post-acute care effectively. Many successful ACOs credit these efforts for allowing them to achieve shared savings.

CMS does not provide opportunities for Medicare ACOs to formally share savings with bundlers, nor does the agency properly incentivize ACOs and bundlers to partner in coordinating beneficiary care. In fact, the rules guiding shared savings in the bundled payment programs specifically preclude an ACO from receiving payments for savings achieved in the bundled payment programs. While the agency encourages collaboration, it has not required it nor given proper incentives for bundled payment participants to enter into agreements with ACOs. Many ACOs report significant challenges negotiating arrangements with bundled payment participants, who have little incentive to do so. Unless bundled payment participants and ACOs sign collaborative agreements, ACO patients’ care should not be included in bundles. The overlap of these models also makes it very difficult to evaluate their separate outcomes, which will become increasingly important as CMS considers which models to expand and focus on in the future.

Summary of Policy Recommendations and Conclusion

The issues included in this white paper are of the utmost importance to ACOs, including those of today and the future. Addressing these challenges will not be easy but is essential to securing the foundation of Medicare ACOs. In summary, we urge CMS and the Administration to:

- Account for the significant investments ACOs make by including them in calculations of ACO risk,

- Address the growing evidence that the current two-sided ACO risk models are not attractive for most ACOs and set the bar much too high in terms of financial risk,

- Work closely with the ACO community to consider new approaches to risk that are more appropriate for the typical Medicare ACO,

- Finalize a list of Advanced APMs under MACRA that includes all Medicare ACOs, including those in MSSP Track 1,

- Remedy issues related to the overlap of Medicare bundled payment programs by prioritizing population-focused total cost of care models and exclude ACO beneficiaries from bundled payment programs unless a collaborative agreement exists between the bundler and ACO, and

- Clarify in regulation that even though ACOs are technically not providers, they are permitted to share in the savings from bundled payment programs where agreements with bundlers exist.

These recommendations reflect our expectation and desire to see Medicare ACOs achieve the long-term sustainability necessary to enhance care coordination for beneficiaries, lower the growth rate of health care spending, and improve quality in the Medicare program.

Appendix A: ACO Risk Structures

|

Downside Risk Element |

MSSP Track 1 (no downside risk) |

MSSP Track 2 |

MSSP Track 3 |

Next Generation ACO Model |

Pioneer ACO Model |

|

Minimum Savings Rate (MSR) /

Minimum Loss Rate (MLR) |

2.0% to 3.9% MSR depending on number of assigned beneficiaries

MLR not applicable to Track 1 ACOs |

Choice of a symmetrical MSR/MLR: no MSR/MLR; symmetrical MSR/MLR in 0.5% increments between 0.5% ‑ 2.0%; symmetrical MSR/MLR to vary based upon number of assigned beneficiaries (as in Track 1) |

Same as Track 2 |

Next Gen does not utilize MSRs/MLRs. Instead, CMS applies a discount to the benchmark once the baseline has been calculated, trended, and risk adjusted. Therefore, Next Gen ACOs can achieve first dollar savings for spending below the benchmark and are accountable for first dollar shared losses for spending above the benchmark. |

1% MSR/MLR (may be up to 2 to 2.7% for Pioneer ACOs in certain payment options) |

|

Shared Loss Rate |

Not applicable |

First dollar losses once MLR is met/exceeded. Shared loss rate may not be less than 40% or exceed 60%. |

First dollar losses once MLR is met/ exceeded. Shared loss rate may not be less than 40% or exceed 75%. |

First dollar shared losses for spending above the benchmark. |

First dollar losses once MLR is met/ exceeded. |

|

Loss Sharing Limit |

Not applicable |

Limit phases in over 3 years, starting at 5% in Year 1; 7.5% in Year 2; and 10% in Year 3 and subsequent years. |

15% |

15% |

Starts as low as 5% in Year 1 in two of the five payment arrangements. The other three start at 10%. All increase over time to 15% in Years 3-5. |

Suggested Citation: National Association of ACOs. (2016). ACOs at a Crossroads: Cost, Risk and MACRA White Paper. Available from www.naacos.com